2026-03-03

The State Social Insurance Reserve Fund (‘the Reserve Fund’) is intended to ensure the financial stability and continuity of the State social insurance system. In other words, the reserve today acts as a tool for cyclical stabilisation – it is built up in good times, when the economy is growing and the annual revenue of the State Social Insurance Fund (SSIF) exceeds expenditure, and it is used when the current revenue for social benefits is insufficient, for example in times of economic downturn. This way of managing social security finances keeps pensions and social benefits stable in bad times and prevents temporary cyclical revenue from being turned into permanent liabilities. The amount of the reserve fund established by law is to accumulate the amount of the expenditure of the SSIF for the previous year. At the end of 2025, the reserve fund amounted to around EUR 4.5 billion, which represents almost 64% of the SSIF expenditure in 2024.

AUTHOR

Jaroslav Mečkovski

Principal Economist, Budget Monitoring Department

el. p. [email protected]

At first glance, this accumulated amount seems significant, but the fundamental question is whether it will be enough to manage future challenges. Sadly, a short and clear answer would be no. The initial purpose of the reserve is to cover a temporary shortage of resources for social security benefits, but the amount currently accumulated is not sufficient to cover the long-term commitments made. For long-term risks, a separate reserve is not built up. Let's look at what makes such an assessment.

One of the most important long-term challenges for the social security system is the inevitable ageing of the population. This is not a cyclical fluctuation, but a structural break. The Independent Fiscal Institution (IFI) projects[1] that even with positive net migration (when more people arrive than leave), Lithuania's population will decrease and could reach 2.6 million in 2050. This is due to the already unfavourable population structure and low birth rate. Looking at the structure of the population, it can be seen that already in the next few years the social security system will become strongly affected by the growing number of pensioners. Currently, one of the largest cohorts of the Lithuanian population is aged 60-64. In 2025, more than 3 people of working age supported one elderly person, and this number is expected to decrease to 2 by 2050.

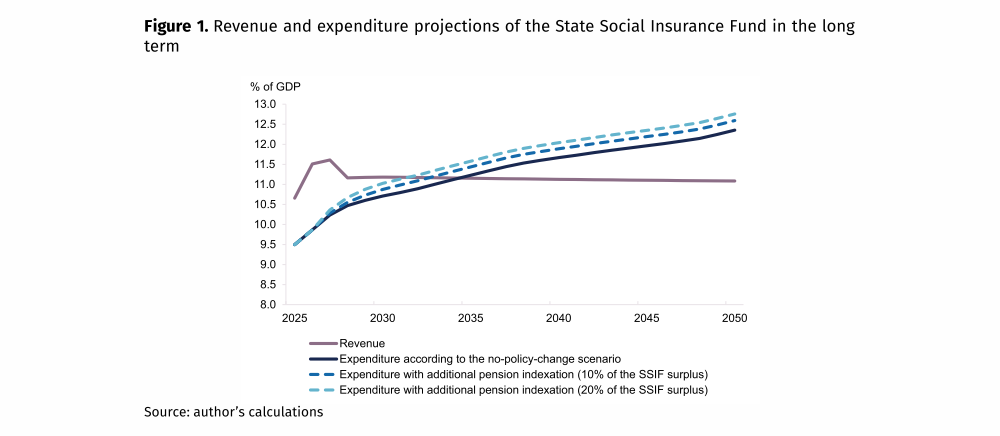

In the long run, as the population ages, pension expenditure will increase and a permanent (structural) deficit of the SSIF will begin to form. The calculations[2] assume that the revenue of the SSIF will increase over the projection period at the rate of wage bill growth, therefore the revenue-to-GDP ratio will remain relatively stable over time (Fig. 1). The increase in the expenditure-to-GDP ratio of SSIF is mainly due to the growing number of old-age pension beneficiaries. Under a no-policy-change scenario (where the revenue and expenditure forecast for 2026-2028 is based on the draft budget of the SSIF for 2026), the revenue of the SSIF will exceed the expenditure until 2034. Later, a deficit will begin to form, which will grow as old-age pension expenditures increase. Accordingly, the resulting deficit would be financed at the expense of the cyclical buffer. Fiscal discipline is a priority, but it is important not to ignore other social aspects. The pension replacement rate is estimated to be around 47-50%. This means that there would be almost no room for reducing the risk of poverty among people of retirement age.

An additional indexation of the individual part of the pension for several years would bring forward the creation of a deficit in the SSIF. When analysing the SSIF expenditure in the long term, two other scenarios were assessed. In both cases, an additional indexation of the individual part of the social insurance pension from 2027 is provided for, allocating 10% and 20% of the planned budget surplus of the SSIF respectively. According to the calculations made, additional indexation would result in an earlier formation of the SSIF budget deficit than under a no-policy-change scenario (Fig. 1). Additional indexation of the individual part, by allocating 10% of the SSIF surplus, would be possible until 2032, because later the budget deficit of the SSIF would start to form. Accordingly, faster indexation (with a 20% of surplus) could take place in an even shorter timeframe.

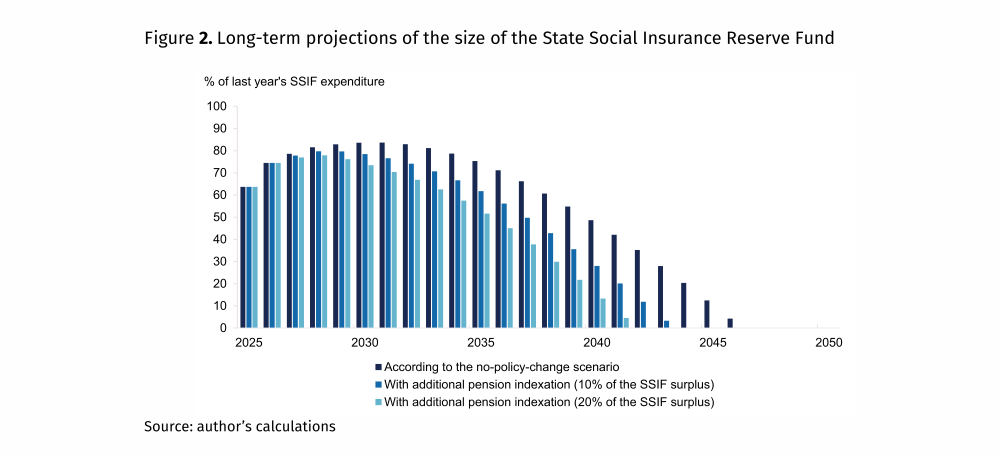

In the long term, the budget deficit of the SSIF will lead to a gradual reduction of the reserve, which would be further accelerated by additional indexation of pensions. Between 2026 and 2028, the size of the reserve is expected to be significantly supplemented by the return of SODRA and State budget contributions from the second pillar pension funds (Fig. 2). Under a no-policy-change scenario, the size of the reserve will continue to increase until 2031, driven by the budgetary surplus of the SSIF. However, as demographic pressures intensify, the size of the reserve will gradually decline and end in 2047. This would mean that, in just over a decade, the instrument that is vital for absorbing unexpected economic shocks (crises) would be fully utilised. In the absence of policy decisions, public debt would have to increase in order to continue to meet the commitments made by the SSIF. Such a situation would be unfavourable in several respects. First, using the reserve to cover demographically-induced structural deficits would reduce the chances of future budgetary stability for the SSIF in times of economic shocks. Second, increased borrowing would negatively affect the sustainability of the country’s public finances in the long term.

A further indexation of the individual part of the pension would accelerate the reduction of the reserve. With the allocation of 10% of the SSIF budget surplus, the reserve would be exhausted by 2044, and with the allocation of 20% - already by 2042. This would be due to two factors. First, the build-up of the SSIF reserve would be slower in the coming years, as part of the SSIF surplus would be allocated to additional pension indexation. Second, additional indexation would increase the replacement rate of pensions, i.e. the long-term liabilities of the SSIF that would need to be financed in the future.

The accumulated reserves will not be sufficient to withstand demographic changes, therefore, it is necessary to look for long-term financing solutions for the SSIF. Estimates show that due to demographic pressure, the reserve fund would be fully exhausted before 2050, regardless of whether a decision is made to introduce additional pension indexation. However, demographic change does not necessarily mean a verdict against the social security system: a breakthrough in labour productivity and GDP growth could, in the long term, mitigate the consequences of an ageing population. A combination of different measures is necessary to meet existing commitments and to avoid neglecting other social objectives, such as reducing poverty among people of retirement age. The Independent Fiscal Institution notes that, in addition to revenue measures, structural reforms are needed, in particular to boost labour productivity and sustainable economic growth. In order to meet existing commitments, it is provisionally estimated that the size of the reserve in 2027 would need to be well above 100% of last year’s expenditure (compared with nearly 64% in 2025) in order to withstand demographic pressures during the period under review. It should be noted that the assumptions in this assessment did not include macroeconomic shocks, which are likely to occur in the long term in the course of economic development cycles. Already now, decisions must not ignore inevitable demographic trends and ensure cyclical stability and the long-term sustainability of the system. Any delay will only further limit the freedom of choice of the state between tax increases and other social objectives.

[1] Internet access: https://www.valstybeskontrole.lt/EN/Product/24298/assessment-of-the-sustainability-of-general-government-finances-in-20252050

[2] The long-term revenue and expenditure projections of the SSIF for this assessment are based on the macroeconomic and demographic assumptions of the IFIs’ assessment of the sustainability of general government finances for 2025-2050.